TL;DR

- AI Payments’ Inaugural Year Opens: Google, jointly with industry partners, released AP2 (Agent Payments Protocol), using authorization mandates + verifiable credentials to bring AI’s proxy transactions on behalf of users into a unified, auditable paradigm.

- Coinbase with Ethereum Community Drives x402: Making API calls equivalent to payments a reality.

- Entrepreneurial Window: AI’s financial world will run parallel to traditional finance for an extended period, creating opportunities for startups. Tech giants are choosing to define open-source protocols in AI payments, but what’s most lacking above these protocols are usable productized components and secure risk control middleware. FluxA starts from

Opening: Tech Giants Racing to Deploy AI Payment—The True Inflection Point Emerges

The AI circle is arguably the most relentless battlefield right now. While the technological giants continue their intense arms race on the model side, a brand new battleground—AI payments—is slowly surfacing. Stripe announced it will launch its own payment L1, Tempo. PayPal announced investment in Kite.AI. And just days ago, Google announced it will launch its own open-source Agent Payments Protocol (AP2) and will collaborate with Coinbase’s previously introduced x402 protocol, integrating x402 into Google’s self-developed A2A framework.

As AI continues to evolve, industry thinking about AI’s capability boundaries and commercialization is gradually entering the next stage. An increasing number of people are recognizing that payment capabilities are indispensable for Agents, because payment is not merely a function. Behind it lies a more fundamental shift: when Agentic AI becomes the “first-class citizen” of the new internet, it will shake the fundamental logic of traditional e-commerce operations, advertising, distribution, and internet finance, while spawning new Agentic Commerce centered on AI.

This article will conduct an in-depth analysis of the latest developments from two giants in the AI payment field: Google’s AP2 and Coinbase’s x402, using these as entry points to analyze development trends and opportunities in AI payments.

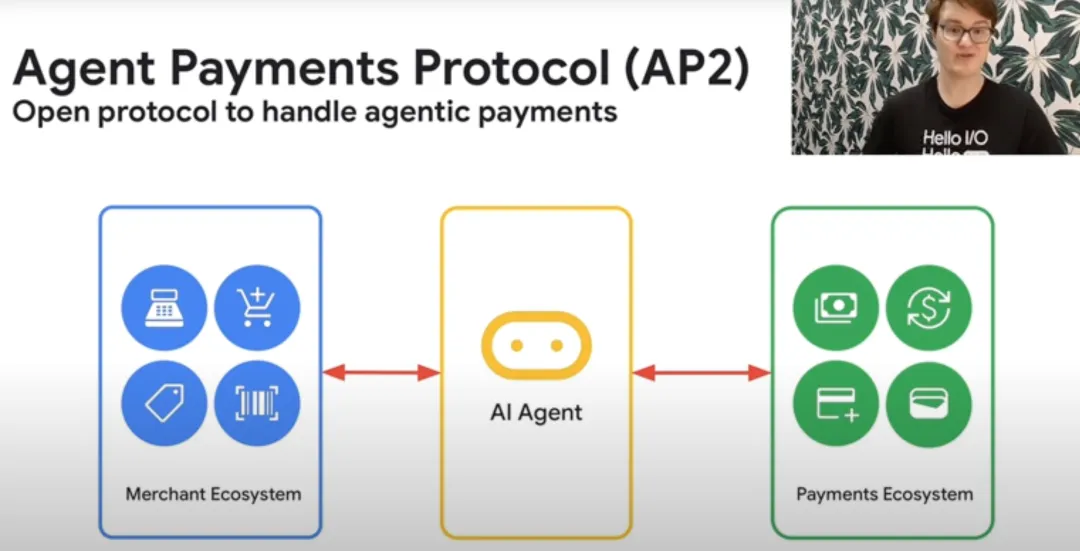

01 | Google AP2: Bringing How AI Spends Money into a Manageable Universal Language

This week, Google jointly released AP2 (Agent Payments Protocol) with over 60 payment networks, financial institutions, e-commerce, and blockchain companies in an attempt to establish unified standards for the intersection of AI and payments.

Before AI, traditional payments were completed when humans clicked “buy” in the payment backend. Any automatic payment behavior not initiated by humans was considered “unsafe” by the entire payment system, which has evolved a mature risk management framework to handle such risks. But in the AI era, this becomes a dilemma: if we allow AI to initiate transactions on behalf of humans, how do we confirm: 1) Whether the user truly authorized the AI to make this transaction? 2) Whether the AI’s request represents the user’s true intent? 3) Who bears responsibility if the transaction goes wrong?

Google’s AP2 addresses this head-on. Google has defined an open protocol standard that serves as a common language for secure and compliant communication between AI and merchants. This is essentially a dual-authorization mechanism between user, AI, and merchant:

- Intent Mandate: The user provides explicit intent: what they want to buy, budget ceiling, and time window.

- Cart Mandate: The agent finds specific products and prices, then requests the user’s signature confirmation again.

Both authorizations are encrypted with verifiable credentials and cryptographic signatures, forming an irrefutable evidence chain after user signature confirmation. For merchants and clearing networks, this means: payment requests don’t come from an unidentifiable robot, but from a user-authorized, verifiable “transaction contract.” Through Google’s defined “transaction contract,” merchants and clearing networks can confidently recognize the legality of the transaction and approve it.

AP2 doesn’t redesign the clearing layer networks like Visa/ACH/stablecoins and blockchain. Instead, it adds a trust semantic layer on top of them—who is spending, what authority they have, and how violations can be traced. This attempts to solve AI payment intent confirmation across different clearing networks like stablecoins and fiat currencies. In traditional payment scenarios, this is initiated by our manual click of the “buy” button, but for AI and the stablecoin era’s “dark forest,” we need cryptography and process constraints to bring every AI behavior into order, ensuring AI won’t harm users’ funds by leveraging its own money-spending power.

While AP2’s design and development are still in very early stages, we can clearly see Google’s focus on AI payments: eliminating concerns from all participants in the Agent payment chain about uncontrollable and unverifiable behavior—this is essential for AI to complete payment behavior:

- For consumers: Authorization defines AI payment boundaries. Budgets, categories, time windows, and exception rules are all crystallized in the authorization. Confirming the agent’s authorized scope before payment. If something goes wrong, it can be traced back to what was authorized, achieving prevention of overreach and post-event appeal capabilities.

- For merchants and payment networks: Upgrading intent confirmation from verbal/interface to cryptographically verifiable intent credentials. Chargebacks and dispute resolution have documented trails, reducing gray losses and compliance uncertainty.

- For the ecosystem: Establishing a common language for AI participation in payments, facilitating multi-party collaborative innovation (identity, risk control, settlement, factoring, etc.) maintaining consistency on the same problem definition.

- For enterprise IT/compliance: Migrating AI-era automated procurement, subscription scaling, and bill payment processes from policy documents + manual review to protocol-level policy execution, with real-time record-keeping that establishes a solid foundation for future penetrating supervision.

02 | x402: Binding Payment to Service, Using Stablecoins to Construct a New Machine Economy

While Google focuses more on authorization and security of AI payments, Coinbase, naturally closer to stablecoins and blockchain, directly extends its hand toward AI’s transaction behavior and settlement itself. Through the x402 protocol promoted with the Ethereum Foundation, Coinbase aims to shape stablecoins and blockchain as the native currency and payment primitives of AI payments, coupling AI’s payment behavior with “consumption” behavior.

x402 draws its name from HTTP 402, which is a status code in the HTTP protocol meaning “payment required to access this resource.” Before the AI and stablecoin era, this status was virtually never standardized throughout history. But the recent rise of AI has shown developers its field of application. As webpage and API access increasingly comes from AI rather than real humans, shouldn’t AI also pay for their access?

x402 addresses this by starting from the payment chain, natively coupling API calls with payments:

When an AI agent calls a service, x402 sends the AI agent an HTTP payment “invoice” based on prepayment information defined by the service provider. The AI agent can then directly complete settlement on-chain using USDC or other stablecoins according to this “invoice,” and the service provider immediately releases the service to the AI.

Though it’s only a simple protocol rather than a complete product, x402 applies stablecoins’ real-time settlement and high programmability to the AI payment scenario, depicting what AI payment might look like and its potential in the stablecoin era:

For AI agents, x402’s existence allows AI agents to complete service calls and payments in one unified process. Leveraging decentralized, highly programmable stablecoin networks, AI no longer needs to follow the human workflow of “binding credit card—initiating payment—waiting for service activation.” Instead, it truly achieves pay-as-you-use. Unlike humans’ relatively low-frequency payment needs, parallelized processing capacity means AI agents’ payment frequency far exceeds humans’. x402 is better suited to AI agents, enabling them to complete finer-grained automated micro-payments and stream payments. AI agents don’t need to pre-register accounts and API keys with various providers; they can automatically negotiate prices when encountering an x402 challenge.

For AI service providers, x402 pushes the “access-as-pricing” capability down to the protocol layer. Future x402 ecosystem developers can fine-grainedly convert pages, APIs, and data chunks into micro-payments, supporting complex payment modes like per-request, per-token, and per-duration billing. Simultaneously, leveraging stablecoins enables instant, cross-border, low-fee settlement. Even with ultra-high transaction volumes, transaction reconciliation becomes effortless.

03 | Two Tracks, Pointing to the Same Destination

If AP2 is AI’s extension of the traditional payment system, x402 is more like the native AI payment prototype of the stablecoin era. When these two converge, they precisely represent how tech giants are jointly weaving the infrastructure across all links of AI Payment, presenting a dual-track parallel scenario: both fiat payments and crypto payments are evolving toward Agent-callable directions.

AP2: Packages real-world regulation, risk control, and consumer protection into Agent transactions.

x402: Packages Web3’s instant settlement and programmability into Agent transactions.

The conclusion is clear: the next stage of AI Payment won’t be either-or, but dual-track parallel and interoperability:

Users and merchants gain compliance and trust under AP2. Computing power/data/microservices gain speed and programmability under x402. Upper-layer products need unified abstraction, seamlessly orchestrating both tracks for Agent use.

04 | Entrepreneurial Track: Above the Protocol. The Missing Executable Layer Product

Tech giants typically start by defining standards to build ecosystems and influence, but “standards” like x402 and AP2 are actually vastly distant from truly usable AI payment products in real environments. Building usable, scalable productized components above the protocol is precisely where entrepreneurs in this track should focus.

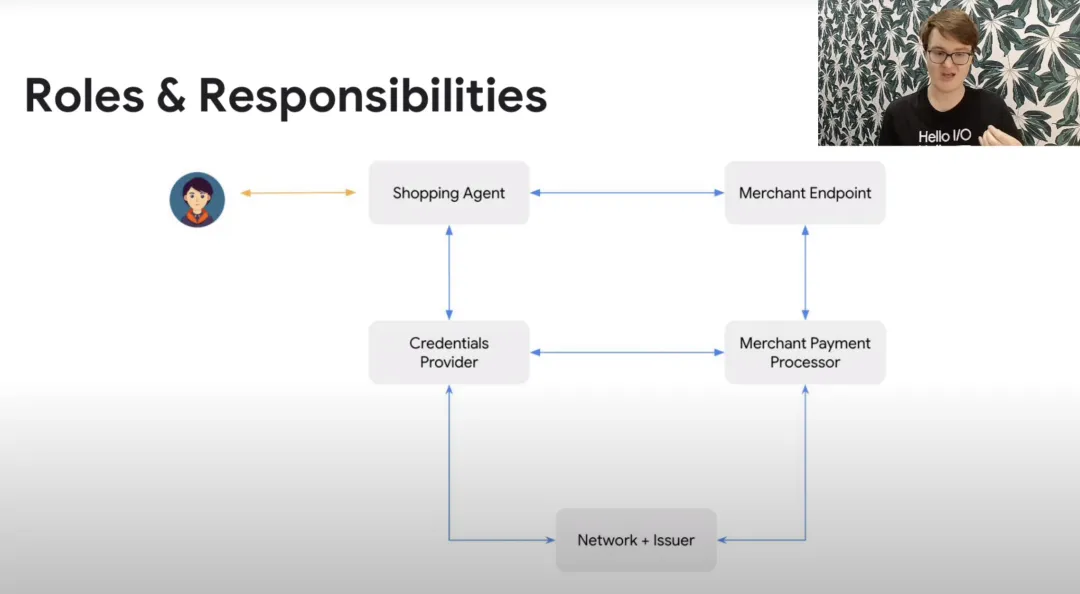

Google summarized multiple participant roles and responsibilities involved in Agent payment processes. Protocols like AP2 primarily coordinate how multiple parties in the payment chain trust AI Agent payment requests through credential verification. We can see that AP2 is not the execution layer of payments—Google chooses to open the execution layer to other payment participants to build together.

Three major roles constitute the payment execution layer: Credentials Provider, Merchant Payment Processor, and Network/Issuer. In the Agent payment era, whether the execution layer can spawn the next trillion-dollar market and players is what AI innovation pioneers are seeking answers to.

05 | FluxA: Building the Mass-Produced Vehicle Above the Protocol

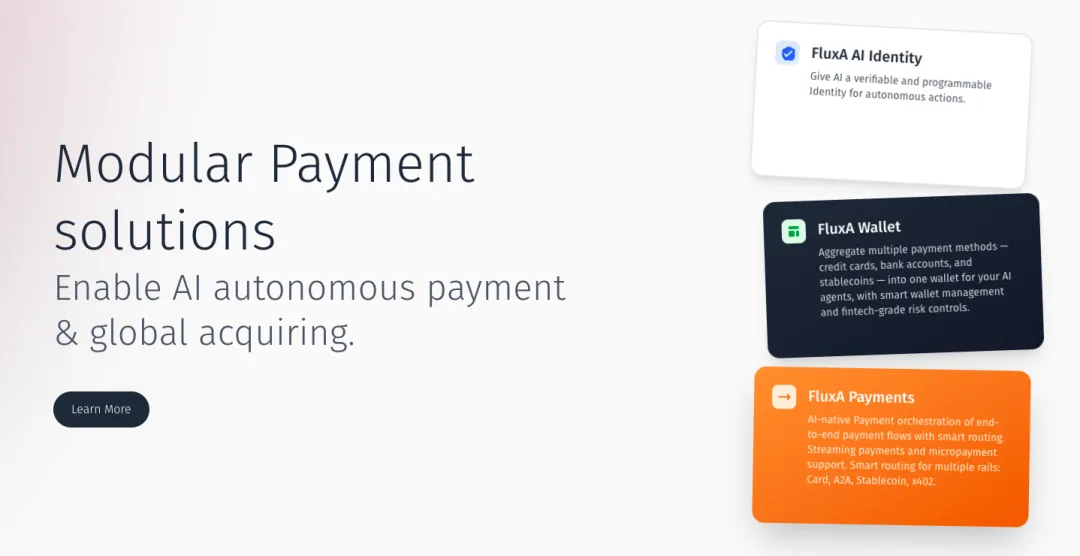

FluxA is an AI-Native payment execution layer. The founding team comes from Alibaba and Ant Group former executives and is actively joining this Agent payment race.

FluxA aims to build a payment primitive for Agent economy, abstracting identity, wallets, and payments into modular primitives. Developers can assemble their own Agentic economic services like building blocks using components provided by FluxA.

FluxA’s core product covers four essential links in AI Agent payments: identity, wallet, acquiring, and payment channels.

- AI Wallet: Aggregates all AI-callable payment methods (bank cards, e-wallets, stablecoin wallets, etc.) for AI Agents, providing a unified payment entry point. Security and risk control modules are the focus, ensuring AI Agents conduct proxy consumption within user intent.

- AI Identity: AI wallets naturally provide trustworthy AI identity IDs for AI Agents, including not only user information authentication but also AI Agent execution authentication. Based on FluxA’s AI identity, merchants and downstream payment participants can further enhance risk control, avoiding risk exposure from providing programmable interfaces for AI Agents.

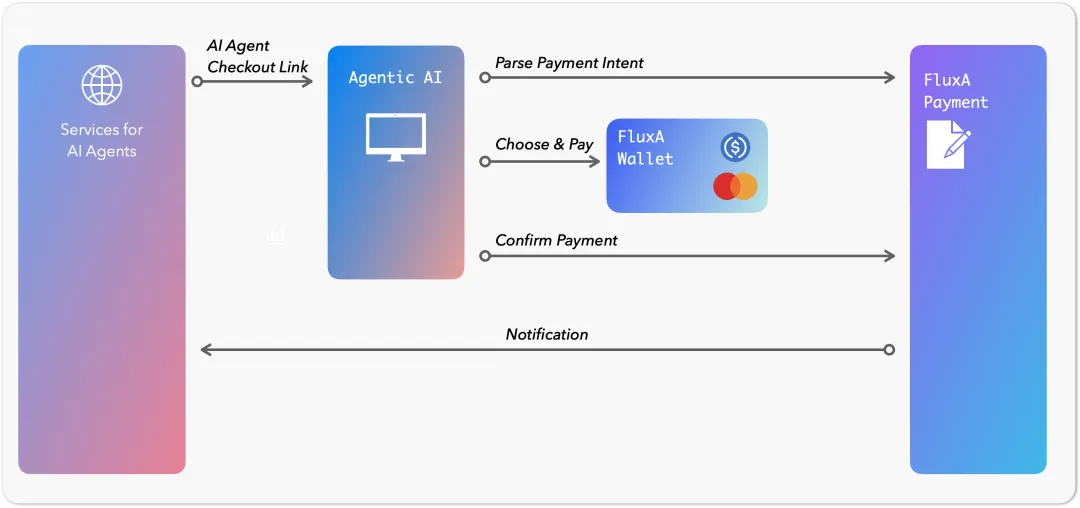

- AI Payment: Provides merchants service for collecting payments from AI Agents. FluxA AI Payment’s core approach is aggregating acquiring—combining multiple payment channels usable by AI Agents, so merchants needn’t worry about AI agents being unable to complete payments. Simultaneously, it integrates industry protocols like AP2 and x402, providing diverse AI-native payment methods.

- Stablecoin Rail: Stablecoins are in early mainstream adoption stages, with many detailed service improvements needed in consumer wallet adoption and merchant acceptance. FluxA will build a seamless stablecoin channel around mainstream compliance and low-threshold adoption, specifically serving AI payments.

If Google AP2 and Coinbase x402 provide the superhighway, FluxA aims to be the first batch of mass-produced vehicles on that highway:

- Connecting with AP2, x402, and other protocols → ensuring compatibility with global payment standards.

- Providing SDK/API → allowing developers to quickly enable AI payment capabilities without researching underlying protocols.

- Targeting application scenarios → whether B2B SaaS automated procurement or C-side Agent e-commerce shopping, FluxA can serve as the payment execution layer.

In early innovative tracks, entrepreneurs often take exploration’s first steps faster than giants. Open protocols are just getting started, and truly usable products remain scarce in the market. Enterprises, on one hand, hope to quickly onboard AI to payment capabilities, but must ensure the process is fast yet orderly—they urgently need compliant, auditable implementation platforms. Simultaneously, developers are unwilling to exhaust themselves integrating with dozens of gateways or wallets; what they need is a unified abstraction layer that makes payment capabilities as simple and direct as API calls.

FluxA won’t create protocols itself, but deeply aligns with and closely follows AP2 and x402’s evolution pace, prioritizing mainstream payment service providers and wallet ecosystem compatibility. FluxA’s value lies in filling gaps: converting protocols into truly usable products, transforming standards into deployable business capabilities, and internalizing security requirements as default configurations. This way, giants handle rules-setting and building superhighways, while entrepreneurs pioneer mass-producible vehicle models on that superhighway.

Payment itself is a vast ecosystem. Creative companies and giants aren’t in opposition but complementary:

- FluxA won’t create protocols but deeply aligns, closely following AP2/x402 evolution pace and prioritizing mainstream payment service providers and wallet ecosystems.

- FluxA’s value lies in occupying an ecological niche: converting protocols to products, transforming standards into operational businesses, and making security requirements default built-ins.

Conclusion: From Dialogue to Transactions, AI Economy Truly Launches

When Google and Coinbase push forward on their respective tracks, establishing protocol standards, what the market needs is no longer new slogans but the execution capability to boldly pioneer implementation. AP2 provides safeguards for compliance and trust; x402 opens space for instant settlement and programmability; while FluxA converts these abstract standards and protocols into truly callable payment primitives and genuinely usable product components.

The next stage of AI Payment will be defined jointly by standards and execution-layer products. Agents not only need to be granted permissions but must be verifiable and accountable. Payment processes aren’t merely executing a single transfer but orchestrating, observing, and extending. For developers, the ideal state is being able to rapidly integrate and launch AI payment/collection capabilities within days.

The inflection point has arrived. FluxA hopes to work with ecosystem partners to advance Agent economy from papers and demos into trustworthy, usable, and scalably operational real-world applications.

FAQ

What is Google AP2 (Agent Payments Protocol)?

AP2 is an open protocol released by Google with 60+ industry partners that establishes unified standards for AI agents making payments on behalf of users. It uses a dual-authorization mechanism — Intent Mandate (user states what to buy, budget, and time window) and Cart Mandate (agent finds products, user confirms) — with cryptographically signed verifiable credentials.

What is Coinbase x402 and how does it work?

x402 is a payment protocol named after HTTP status code 402 ("Payment Required") that couples API calls with stablecoin payments. When an AI agent calls a service, x402 sends an HTTP payment invoice, the agent settles on-chain using USDC, and the provider immediately releases the service. It enables true pay-as-you-use for AI agents.

How do AP2 and x402 complement each other?

AP2 focuses on authorization and compliance — packaging regulation, risk control, and consumer protection into agent transactions. x402 focuses on settlement — packaging instant programmable stablecoin payments into agent transactions. Together they form a dual-track system: fiat compliance through AP2, crypto speed through x402.

What is FluxA's role in the AI payments ecosystem?

FluxA builds the payment execution layer above protocols like AP2 and x402. It provides modular primitives — AI Wallet, AI Identity, AI Payment, and Stablecoin Rail — that let developers quickly enable AI payment capabilities without implementing underlying protocols directly.

Why do AI agents need their own payment infrastructure?

Traditional payment systems were designed for humans — they rely on visual interfaces, manual approvals, and anti-bot risk controls. AI agents can't click buttons, wait for verification codes, or scan QR codes. They need machine-native payment protocols that support high-frequency micropayments, programmatic authorization, and real-time settlement.