AI Is Now Doing Your Shopping For You

You open five tabs. You compare the same product across three retailers. You re-enter your shipping address. You read 47 reviews and still feel uncertain. Then you abandon the cart.

This is the reality of modern e-commerce — and it hasn't fundamentally changed in 20 years. The interface got prettier. The checkout got slightly faster. But the cognitive load still falls entirely on you.

Agentic commerce changes that equation completely.Instead of you navigating the store, an AI agent navigates it for you — researching options, filtering by your preferences, and completing the purchase without requiring your attention at every step.This isn't a chatbot. It's a shift in who does the work.

TL;DR

Agentic commerce is an AI-driven model in which autonomous agents research, compare, and complete purchases on behalf of consumers or businesses — without direct human intervention at each step.

| What changed | AI agents can now reason, plan, and transact across platforms — not just recommend |

| Two layers | Discovery (Google, Shopify, Amazon) + Payment (FluxA AgentCard, AEP2) |

| The gap | Discovery is largely solved — the payment layer is where most implementations break down |

| Key risk | Agents with open credit card access are a liability; spend controls and single-use credentials are the baseline |

| Who benefits now | Consumers, B2B procurement teams, and developers monetizing APIs and MCP servers |

| Market signal | McKinsey projects $3T–$5T global opportunity by 2030; 20% of 2025 Cyber Week orders already AI-influenced |

Our take: Agentic commerce isn't just a feature upgrade — it's the end of passive e-commerce. The discovery layer is largely handled. The payment layer is where the real work is.

Why Agentic Commerce Is Possible in 2026

The technology finally caught up

For years, "AI shopping" meant algorithmic product recommendations — useful, but ultimately reactive. What's different today is that large language models have crossed a capability threshold that makes goal-oriented, multi-step action reliable at scale.

The duration of tasks that LLMs can reliably complete has been doubling roughly every seven months since 2019. In practical terms: early models could handle a single-step lookup. Today's agents can manage an entire purchase workflow — from requirement gathering to checkout confirmation — without human input at each stage.

At the same time, open API ecosystems have matured. AI agents can now interface directly with retailer inventory systems, payment processors, and user preference data in real time — the infrastructure that makes agentic action possible didn't exist at this scale three years ago.

How agentic commerce actually works differently

Unlike traditional e-commerce experiences — which require a person to manually search for products, compare options, read reviews, and complete checkout step by step — agentic commerce shifts much of that work to AI agents.

These agents don't wait to be asked. Unlike chatbots or simple automation tools that only respond to prompts, agentic systems proactively plan and execute actions on behalf of the customer. The distinction matters: a chatbot answers your question; an agent solves your problem.

Agentic commerce is also not limited to online shopping — it applies to travel and ticketing, subscriptions and digital services, and physical retail integrations.

Current limitations and trust guardrails

Agentic commerce is not a fully autonomous free-for-all — and it shouldn't be. Most implementations today operate within explicit permission boundaries set by both merchants and consumers. Governance controls such as permissions, audit logs, and fraud safeguards are essential for enabling AI agents to operate safely at scale.

Regulatory frameworks around agent identity — often called "Know Your Agent" (KYA) — are still catching up to the technology. Until those standards solidify, the most responsible implementations keep humans in the loop for high-value or irreversible transactions.

This is precisely where tools like Fluxa matter: purpose-built agentic commerce infrastructure includes trust layers by default, so brands don't have to bolt on compliance after the fact.

The market signal is clear

McKinsey projects the global agentic commerce opportunity at $3 trillion to $5 trillion by 2030, with up to $1 trillion in US B2C retail alone. Meanwhile, retailers that deployed AI capabilities saw 14.2% sales growth between 2023 and 2024, compared to 6.9% for those without.

The gap between early movers and laggards is already measurable. It will only widen.

How Agentic Commerce Actually Works: Discovery and Payment

Most conversations about agentic commerce focus on the discovery side — how agents find, compare, and decide. That part is largely solved. The harder problem is what happens next.

The Discovery Layer: How Agents Find and Choose

The major platforms have already built agentic discovery into their existing surfaces. Google's Gemini surfaces products directly inside conversational search. Shopify's AI layer reads merchant catalogs and guides shoppers through checkout. Amazon's Rufus handles product discovery and comparison natively inside the app.

This is where most consumers will first encounter agentic commerce — not through a separate app, but through platforms they already use daily.

What it does well

- Handles product research, comparison, and recommendation autonomously

- Works within platforms consumers already trust

- No separate app or interface required for the end user

Where it falls short

- Agent can decide what to buy, but cannot complete the transaction independently

- No cross-platform payment capability

- Merchant has limited control over how agents rank or present their products

For merchants, the practical implication is clear: your product data, pricing, and inventory need to be structured and machine-readable, because agents are now the ones evaluating them — not humans skimming a page.

The discovery layer is maturing fast. But it has a hard ceiling. An agent can identify the right product, compare options, and decide and then it gets stuck. Because deciding to buy and actually paying are two completely different problems, and how autonomous agents pay turns out to be the harder one.

The Payment Layer: Where Most Implementations Break Down

Giving an AI agent access to your real credit card is not a solution. A compromised agent with exposure to your full credit line, no automatic audit trail, and no per-task spending limits is a liability, not a feature.

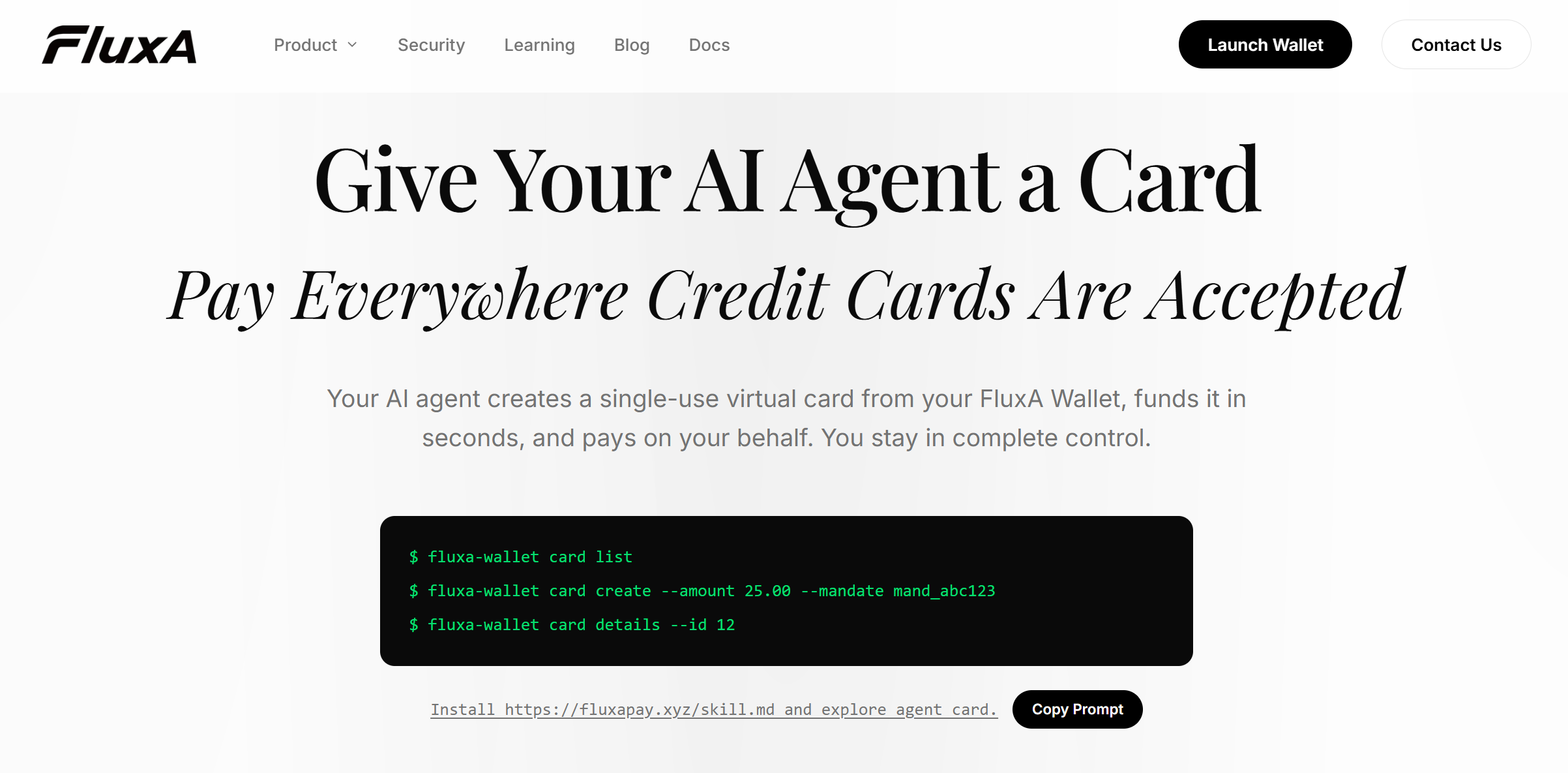

This is the gap that FluxA was built to close. FluxA is a payment layer designed specifically for AI agents, built around the architecture and protocols agent payments actually need rather than adapted from consumer fintech.

How FluxA works

When an agent needs to make a purchase, it issues a single-use AgentCard from your FluxA Wallet — a virtual card funded for exactly that one transaction. Once the payment settles, the card closes automatically. Unused balance returns to your wallet. The agent never touches your real credentials, and every transaction is logged with the agent's identity and mandate context.

For more complex workflows — agents paying for API calls, MCP services, or high-frequency micropayments — FluxA's AEP2 protocol lets agents embed payment mandates directly inside agent-to-agent or MCP calls. The model is authorize first, settle later: transactions clear instantly without the latency of traditional payment rails.

What it does well

- Agent never accesses your real card or full credit line

- Each AgentCard is amount-locked, single-use, and auto-closes after the task

- Full audit trail per agent, per transaction

- Supports high-frequency micropayments and cross-agent workflows via AEP2

- KYC/KYB/KYA compliance built into the protocol layer

Where it fits

- Any team deploying agents that need to complete real purchases

- B2B procurement workflows running across multiple platforms

- Developers monetizing MCP servers and APIs with agent-native payments

Why Both Layers Matter

| Discovery Layer | Payment Layer | |

|---|---|---|

| Function | Find, compare, decide | Execute, settle, audit |

| Tools | Google Gemini, Shopify AI, Amazon Rufus | FluxA Wallet & AgentCard |

| Solved by | Platform-native AI | Purpose-built agent infrastructure |

| Without the other | Agent decides but can't pay | Payment layer with nothing to buy |

Discovery without payment is just a smart search engine. Payment without discovery is infrastructure with no front door. Agentic commerce only works when both layers are in place — and right now, the discovery layer is largely handled. The payment layer is where the real implementation gap sits.

Staying in Control While Letting Agents Act

Agentic commerce introduces a question that traditional e-commerce never had to answer: what happens when the buyer isn't human?

The efficiency gains are real. But so are the risks — and the brands that scale agentic commerce successfully will be the ones that treat trust and governance as infrastructure, not afterthought.

Who Is Actually Responsible When an Agent Transacts?

This is the question regulators, merchants, and payment networks are all working through right now. Emerging frameworks around agent identity — commonly referred to as "Know Your Agent" (KYA) — are pushing toward a model where every agent action is attributable, auditable, and reversible if needed.

Until those standards fully solidify, the practical answer is: you are responsible for what your agent does. That means the guardrails you set upstream determine the risk exposure downstream.

What responsible agentic commerce looks like

- Explicit per-task spending limits, not open-ended access

- Single-use payment credentials that expire after each transaction

- Full audit logs that record agent identity, mandate context, and transaction outcome

- Human approval thresholds for high-value or irreversible purchases

- Compliance coverage for KYC/KYB/KYA at the payment layer

Who Benefits Most Right Now

Agentic commerce isn't equally valuable for every use case today. The clearest wins are in scenarios where the purchasing decision is repetitive, preference-driven, or time-sensitive.

Consumers benefit most from routine replenishment (groceries, household supplies, subscriptions) and time-sensitive purchases where speed matters more than deliberation.

B2B teams benefit from automated procurement — agents that monitor supply levels, compare vendor pricing in real time, and place orders within pre-approved parameters without requiring a human in every loop.

Developers and API providers benefit from agent-native monetization — where other agents discover, evaluate, and pay for services programmatically, without a human-driven checkout flow at all.

What You Can Learn From Early Adopters

The brands seeing the most traction with agentic commerce share three traits. First, they structured their product and inventory data early — agents can only act on information they can read. Second, they separated the discovery layer from the payment layer architecturally, rather than trying to solve both with one tool. Third, they defined agent permissions before deployment, not after the first incident.

The common mistake is treating agentic commerce as a feature to turn on. The brands that do it well treat it as a system to design.

Conclusion

Agentic commerce is not a future scenario. It is the current direction of every major commerce platform, payment network, and AI lab simultaneously. The consumer behavior data from 2025 — 20% of global Cyber Week orders influenced by AI, chatbot traffic to retail sites up 670% year-over-year — reflects adoption that is already happening, not adoption that is coming.

The brands and developers who move now are building on infrastructure that will compound in value as agent-driven commerce becomes the default. Those who wait are not avoiding risk — they are accumulating it.

If you are building agent workflows that need to transact, FluxA is the payment layer designed for exactly that. Start with the AI Wallet, explore the AgentCard for secure single-use agent payments, or read the AEP2 protocol docs if you are building at the infrastructure level.

Frequently Asked Questions

What is agentic commerce in simple terms?

Agentic commerce is when AI agents shop on your behalf — researching, comparing, and buying — without you stepping in at each stage. Think of it as delegating your entire purchasing workflow to an AI that acts on your preferences, not just your prompts.

How is agentic commerce different from a shopping chatbot?

A chatbot responds when you ask. An agentic system acts without being prompted — it plans, executes multi-step tasks, and completes transactions end-to-end. The difference is between answering a question and solving a problem autonomously.

Is agentic commerce safe?

Safety depends on the payment infrastructure behind it. Agents with open access to real credit cards are a liability. Purpose-built tools like FluxA use single-use, amount-locked virtual cards so agents transact only within boundaries you define.

What is a KYA framework?

KYA (Know Your Agent) is the agent-era equivalent of KYC. It applies identity verification and accountability requirements to AI agents, ensuring every agent transaction is attributable and auditable — not just the humans authorizing them.

Do I need to be a developer to use agentic commerce tools?

Not always. Platform-native tools from Google, Shopify, and Amazon need no technical setup. Infrastructure tools like FluxA target teams running agent workflows, but onboarding is lightweight and well-documented.

What industries are adopting agentic commerce fastest?

Retail leads, but adoption is broad. B2B procurement, travel, subscriptions, and API-driven services are all moving fast — anywhere purchases are repetitive, preference-driven, or time-sensitive enough to remove the human from the loop.