AI agents can already write code, browse the web, and manage your calendar — but the moment they need to pay for something, the loop breaks. An AI agent wallet is the infrastructure layer that closes that gap.

TL;DR

What it is: An AI agent wallet is a programmable payment layer for autonomous software.

What it does:

- Lets AI agents send, receive, and manage digital funds independently

- Combines programmable payment infrastructure with agent-readable spending policies

- Enables real-time transactions within limits you define

What it replaces: Manual human approval on every financial action your AI takes.

What is an AI agent wallet? (And why does it matter now)

AI assistants can already write code, browse the web, book meetings, and analyze documents on your behalf. But the moment one of them needs to pay for something — an API call, a microtransaction, a smart contract settlement — the autonomous loop breaks. You get a notification. You pick up your phone. You approve manually. The agent waits.

That interruption is not a minor friction point. It is the structural gap between AI that assists and AI that acts. An AI agent wallet exists to close it: giving software the ability to transact on its own, within predefined boundaries, without constant human sign-off.

The core problem it solves:

- Traditional wallets require a human to sign every transaction

- AI agents operate asynchronously, at scale, and faster than manual approval allows

- Without autonomous payment capability, multi-step agentic workflows stall at every financial action

Background: why standard wallets are not built for agents

Every standard digital wallet is designed around one assumption: a human is present at the moment of signing. That design is intentional and correct for personal finance. It keeps custody and authorization entirely with the user.

AI agents break that assumption. They run asynchronously, across time zones, often executing dozens of actions per minute. Consider:

- A SaaS management agent that needs to process subscription payments across 50 accounts per hour

- A research bot paying per-query to a premium data API in real time

- A supply chain agent settling micro-invoices on your behalf without delays

None of these workflows can tolerate a manual confirmation step. The agent needs to act — and the infrastructure needs to allow it safely.

How to Set Up an AI Agent Wallet: 2 Methods

There's no single right answer for giving an AI agent payment capability, and FluxA, Skyfire, Coinbase, and Crossmint each take a different route. The right method depends on one question: is your agent spending its own funds, or acting on behalf of a human user?

Method 1: FluxA AI Wallet (Recommended for autonomous agents)

Best for: Agents that operate independently — calling paid APIs, purchasing data feeds, settling micro-invoices, or executing workflows without a human in the loop.

The problem it solves:

Your agent runs at 2am, needs to pay for an API call, and there's no one available to approve it. Traditional payment infrastructure stalls here. FluxA is built specifically for this gap: the agent holds its own funds, operates within rules you define once, and never interrupts you for routine transactions.

How it works:

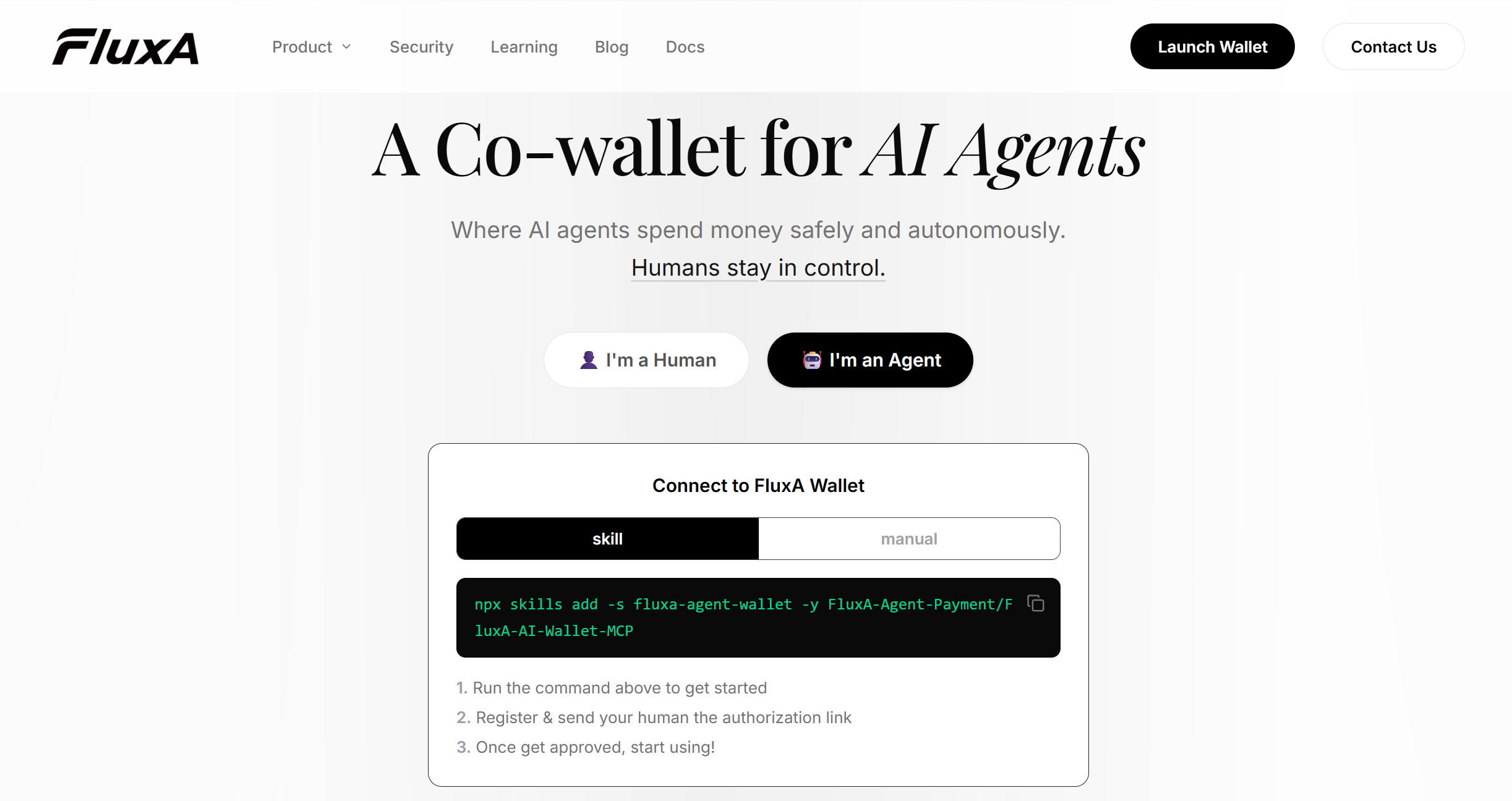

FluxA runs on an authorize-then-act model — you set the policy once, your agent handles everything within it.

Step 1 — Authorize. Grant your agent a FluxA Agent ID and approve wallet access via a one-click URL. Set a spending budget and choose your policy: per-transaction approval, or pre-authorized within a scoped time window.

Step 2 — Transact. The agent pays autonomously within your limits — via x402 payments, single-use AgentCards, or direct payouts — without interrupting you.

Step 3 — Audit. Every payment is automatically logged with agent identity, mandate context, and timestamp. Full audit trail available from your dashboard anytime.

Key features:

- Spend limits — per-transaction caps and daily budgets, adjustable anytime

- AgentCard — single-use virtual cards, auto-invalidated after each transaction

- TEE hardware security + Privy non-custodial base layer

- Built-in real-time risk control against hallucinations and prompt injection

- One-click revocation — no code changes needed

Pros:

- Agent holds its own funds — no human account required

- Infrastructure-level spending controls, not code-level guardrails

- MCP-native, works with Claude Code, Codex, OpenClaw and more

- Ready in under 5 minutes

Cons:

- Stablecoin base layer (USDC) — not designed for traditional fiat flows

- Greatest value within MCP and agent-native ecosystems

Best for: Any autonomous agent that needs to spend money independently — on APIs, tools, data, or services — without waiting for human approval each time.

Method 2: Stripe Shared Payment Tokens (SPT)

Best for: Agents that shop or book on a human user's behalf, charged to the user's saved payment method.

The problem it solves:

You're building a consumer-facing product — a shopping assistant, a travel booking agent, a personal finance tool — where the agent acts on a user's behalf and the cost should appear on their card, not a shared wallet. The agent doesn't need its own funds. It needs delegated access to a human's payment method, scoped and revocable.

How it works:

Stripe's Shared Payment Tokens let an agent initiate purchases using a human user's saved card — without ever exposing the underlying credentials. The agent is a purchasing proxy; the buyer's identity and payment method stay entirely within Stripe's infrastructure.

Step 1 — Connect. Install the Stripe Agent Toolkit and configure your API keys.

Step 2 — Delegate. The human user authorizes the agent to act on their behalf. Stripe issues a scoped SPT — bounded by merchant, time, and amount, monitored via webhook.

Step 3 — Purchase. The agent completes transactions on the user's behalf. Stripe handles checkout, tax, and fulfillment via the Agentic Commerce Suite.

Key features:

- SPTs scoped by merchant, amount, and time — monitored via webhook in real time

- Stripe Radar fraud screening on every transaction

- Already live with Etsy and URBN (Anthropologie, Free People, Urban Outfitters)

Pros:

- Right model for consumer-facing products — agent charges the user's card directly

- Familiar infrastructure for teams already running Stripe billing

Cons:

- $0.30 fixed fee per transaction — makes micropayments economically unviable

- Agent does not hold its own funds; requires a linked human account

- No independent agent policy engine — controls depend on token scope only

- Not designed for autonomous agent-to-API payments

Best for: Consumer-facing agents buying on a user's behalf. Not the right fit for autonomous agent workflows or API micropayments — for those, see Method 1.

At a Glance

| FluxA AI Wallet | Stripe SPT | |

|---|---|---|

| Agent holds own funds | ✅ | ❌ |

| Micropayments | ✅ fractions of a cent | ❌ $0.30 floor |

| Spending controls | Infrastructure-level policy engine | Token-scope within Stripe infrastructure |

| MCP-native | ✅ | ✅ (mcp.stripe.com) |

| Audit trail | Automatic, agent-identity tagged | Webhook monitoring per token |

| One-click revocation | ✅ | ✅ per token |

| Payment methods | USDC / stablecoin | Cards, BNPL, digital wallets |

| Fraud protection | TEE + real-time risk controls | Stripe Radar |

| Best for | Autonomous agent workflows | Consumer purchasing agents |

The distinction that matters: FluxA and Stripe SPT aren't solving the same problem, and a closer look at Crossmint, Nevermined, and FluxA shows how differently the agent-native wallets handle the same job. If your agent needs to act independently — calling services, paying for tools, running overnight without supervision — FluxA is the right layer. If your agent is a purchasing proxy for a human user, and the charge belongs on their card, Stripe SPT is the right architecture. Choosing the wrong one means either building payment guardrails you shouldn't have to maintain, or deploying an agent wallet where a human's payment method was always the right answer.

Risk, compliance, and responsible use

The core principle is simple: constrain first, expand later. Never deploy an agent with open-ended payment access. Start with the smallest budget that covers your use case and expand as trust is established.

Four risks worth managing from day one:

- Unbounded spending — per-transaction caps and daily budgets are your first line of defense, not an optional feature

- Credential leakage: never give an agent a root private key, a card number, or a long-lived API key, and use scoped session keys or FluxA's single-use AgentCards instead

- Prompt injection: adversarial content in web pages or API responses can trigger unauthorized payments, which is why agent payments need a new kind of risk control, and FluxA's risk control layer monitors and freezes suspicious activity automatically

- Irreversibility — agent payments cannot always be undone once executed; design spending rules for the worst case, not the average case

On compliance: If your agent touches regulated rails — fiat on-ramps, licensed exchanges, or high-value transactions — KYC obligations may apply under FATF guidelines. FluxA's AEP2 protocol includes optional KYC/KYB/KYA modules for teams that need verified transaction flows. For production deployments, consult legal counsel before launch.

Conclusion

AI agent wallets are live infrastructure in 2026 — not a future concept. The difference between agents that assist and agents that act comes down to one question: can they transact without waiting for you?

FluxA is built specifically for this. Agent identity, spending policy, payment execution, and risk control in a single layer — non-custodial by design, no Solidity required, ready in minutes.

Ready to give your agent payment power?Launch FluxA AI Wallet · Docs · Request a demo

FAQ

What is an AI agent wallet?

An AI agent wallet is a programmable payment layer for autonomous software. It lets AI agents send, receive, and manage digital funds independently — within spending limits and policies defined by the human owner — without requiring manual approval on every transaction.

How is it different from a regular digital wallet?

A standard digital wallet requires a human to sign every transaction. An AI agent wallet adds a policy layer on top: spending caps, scoped session keys, mandate windows, and audit trails. The agent can transact autonomously within those rules — the human stays in control without being in the loop for every action.

Can an agent spend money without my permission?

No — not with a properly configured wallet. With FluxA, agents can only operate within the budget and policy you explicitly set. You can revoke access instantly with one click, no code changes required.

What if my agent gets hacked or behaves unexpectedly?

Your spending limits are the structural constraint — a compromised agent cannot exceed your caps regardless of what instructions it receives. FluxA's risk control layer monitors for unusual patterns and can freeze activity automatically. Revocation takes one click.

Do I need to know how to code to use FluxA?

No. FluxA's dashboard handles wallet setup, agent authorization, and spending policy without any coding. An SDK and full developer documentation are available for teams that want deeper integration.

Is FluxA custodial?

No. FluxA provides software infrastructure only and does not hold or custody customer funds. The base layer is powered by Privy's non-custodial wallet infrastructure — your assets remain under your own credentials at all times.