TL;DR

- Core problem: API keys and OAuth verify access — not delegation chain, action scope, or authorization provenance. They were built for human sessions, not autonomous agents.

- Solution: Verifiable credentials give agents three proofs in one — origin (who issued the identity), delegation (who authorized it and what they approved), and action scope (what it can do right now).

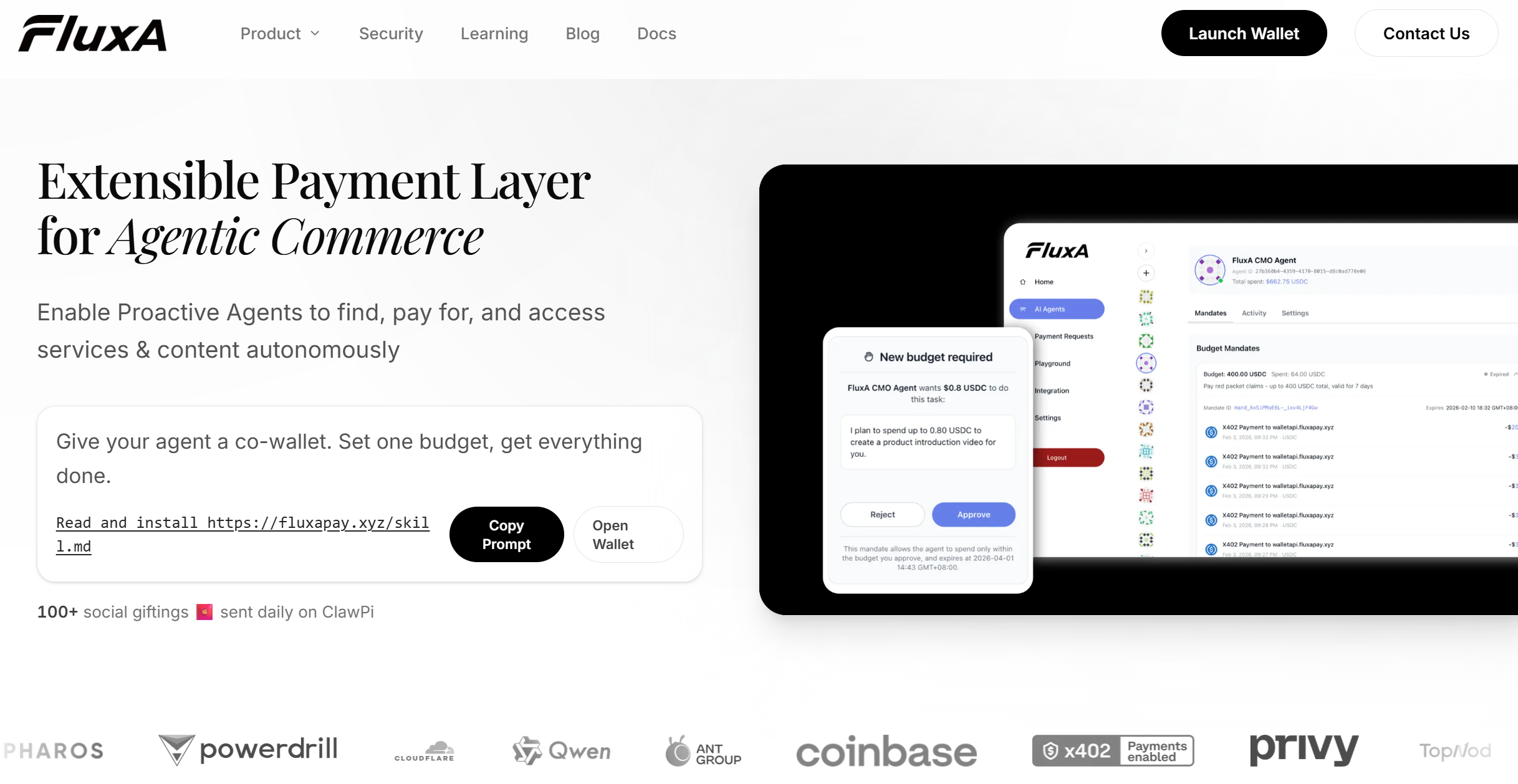

- Implementation: FluxA Agent ID issues

agent_id+token+jwtat registration. A human-signed mandate sets budget, time window, and host scope. Every payment is checked against that mandate before it clears. - Industry signal: Mastercard and Google launched Verifiable Intent (March 2026) as production infrastructure for the same principle. NIST's AI Agent Standards Initiative (February 2026) identifies agent identity as a core regulatory pillar.

What is agent identity, and why does it matter for commerce?

Agent identity is the set of cryptographically verifiable claims that establish an AI agent's origin, delegated authority, and permitted action boundaries — independently of the platform where it operates.

An AI agent booking travel, purchasing API access, or paying a contractor does so without human approval at each step. When that transaction reaches a merchant or payment processor, three questions must be answerable programmatically, and the checks a merchant runs on an incoming agent order map directly onto them:

- Who is this agent, and which system issued its identity?

- Which human or organization delegated authority to it, and what exactly did they approve?

- What is this agent permitted to do in this specific context, right now?

Without verifiable answers to all three, every agent transaction rests on an assumption rather than a proof — commercially significant at scale, and legally significant as regulators begin treating agent-initiated payments as auditable financial events.

Why do traditional authentication methods fail for autonomous agents?

API keys and OAuth tokens verify access. They cannot establish delegation chain, action scope, or authorization provenance — the three things autonomous commerce requires.

The failure is structural, not a configuration problem:

No delegation record.

API keys confirm that something has access. They cannot confirm that a real person authorized the agent to act, under what conditions, or with what spending limits attached. For a deeper breakdown of where this distinction matters in practice, API key vs. AI agent wallet: what's the difference walks through the structural gap between all-or-nothing access and mandate-scoped delegation.

No action boundary.

OAuth scopes define what a credential can access — not what the agent is permitted to do within that access. The difference between a $10 API call and a $3,000 vendor payment is invisible to a token.

No cross-platform portability.

A service account authenticated on Platform A carries no verifiable claims when the same agent operates on Platform B. Each new platform must either extend implicit trust or rebuild verification from scratch, which is exactly the gap we work through in how AI agents authenticate across platforms.

This is why FluxA's security architecture treats every agent payment as a three-party relationship — user, agent, and merchant — where each relationship requires independent verification rather than inherited human-session trust.

What triggered the shift to verifiable agent identity in 2026?

Three forces converged: transaction volume crossed a commercial threshold, institutional infrastructure went live, and the fraud model inverted.

Volume.

According to CryptoNews (April 2026), approximately 69,000 active AI agents on x402 have processed over 165 million transactions totaling $50 million in cumulative volume. At that scale, accountability gaps compound into chargeback disputes and merchant refusals that no policy workaround absorbs.

Institutional adoption.

In March 2026, Mastercard and Google jointly launched Verifiable Intent — an open trust framework that cryptographically links each agent transaction to its human-approved mandate. Mastercard has since rolled out authenticated agentic transactions across Singapore and Malaysia. This is production infrastructure, not a pilot.

Inverted fraud surface.

Traditional fraud detection flags machine-like transaction patterns. In agent commerce, those patterns are the baseline. The real risk is agents executing outside their mandate — triggered by model drift, prompt injection, or reasoning errors. Behavioral heuristics cannot attribute an action to a specific delegation decision. Identity-bound authorization proofs can.

What are verifiable credentials, and how do they differ from tokens?

A verifiable credential is a cryptographically signed attestation about an agent that any counterparty can validate independently — without contacting a central authority.

A token grants access. A verifiable credential proves something: who issued the identity, what the agent is authorized to do, and under whose delegation it operates. The credential travels with the agent. Counterparties verify it on the spot.

According to the W3C Verifiable Credentials Data Model, each credential combines a persistent identifier unique to the agent, signed claims about its attributes and permissions, and a cryptographic proof that makes the credential tamper-resistant and cross-domain verifiable.

How does the three-layer trust model work in practice?

Agent trust operates across three distinct layers — identity issuance, delegation binding, and action-scope enforcement. Each must hold independently for a transaction to be verifiable. These layers are one slice of a wider stack, and the full architecture of AI agent payment systems shows how identity connects to the wallet, authorization, and settlement layers.

Layer 1 — Identity issuance.

An agent registers and receives a credential set: a unique agent_id, a persistent token, and a short-lived jwt. Per FluxA's Agent ID documentation, every agent must complete this registration before it can spend, receive, or manage funds. The JWT is the bearer token attached to every subsequent API call — it is what downstream services check to confirm the agent's identity.

Layer 2 — Delegation binding.

The agent proposes a spending mandate to the human owner: a structured authorization specifying a budget cap, validity window, permitted service hosts, and a plain-language description of purpose. The user signs it once. After that, the agent spends against the mandate without per-transaction approval — the mandate is the cryptographic record of what the human actually authorized. For workloads that span traditional web checkout rather than API calls, disposable virtual cards for AI agents covers how single-use credentials extend the same isolation principle to card-based transactions.

Layer 3 — Action-scope enforcement.

Each payment is checked against an eligible mandate before it clears. FluxA's risk control layer — covering intent consistency, prompt-injection recognition, and behavioral drift — runs continuously across the agent's task chain.

Every action stays attributable to a specific delegation decision. For teams deploying agents into browser-based purchase flows, how FluxA handles AI agent checkout automation shows how scope enforcement extends beyond API calls into real-world checkout sequences.

How does cross-platform identity portability work in practice?

One Agent ID, recognized everywhere — no re-registration, no repeated onboarding.

Per FluxA's agent overview, every agent has a permanent Unify Payment Link (UPL): any counterparty who knows the Agent ID can transact with it directly, even if the underlying wallet address changes. As more of those counterparties are themselves agents, identity starts to carry reputation, which is the case we make for why AI agents need a social graph to pay each other. The credential issued at registration remains the persistent identity anchor across framework migrations and platform switches.

What does agent identity mean for B2B trust?

An agent with verifiable credentials can prove it represents a specific organization — without manual verification.

Mastercard and Google's Verifiable Intent framework creates a tamper-resistant log linking identity, intent, and action into a single record, verifiable by any counterparty independently. A FluxA Agent ID operates on the same principle: the mandate specifies who authorized the agent, under what budget, and for what purpose — the counterparty checks the credential and the transaction proceeds.

Summary

| Layer | What it solves | FluxA implementation |

|---|---|---|

| Identity issuance | Proves agent origin | agent_id + token + jwt via /register |

| Delegation binding | Links actions to human-approved mandate | Budget, time window, host scope |

| Action-scope enforcement | Blocks out-of-mandate transactions | Risk control checks every payment before it clears |

| Cross-platform portability | Single credential across all platforms | Permanent UPL tied to Agent ID, not wallet address |

Agents operating without verified identity accumulate accountability gaps that compound as transaction volume grows. The time to establish identity infrastructure is before autonomous spending begins — not after incidents occur.

Register your agent with FluxA →

Frequently Asked Questions

What is AI agent identity?

A verifiable credential set proving an agent's origin, delegated authority, and permitted actions. Unlike API keys, it establishes who authorized the agent, under what conditions, and within what boundaries.

Why can't API keys authenticate AI agents?

API keys verify access, not authorization. They carry no delegation record, no spending scope, and no cross-platform portability — the wrong foundation for autonomous systems operating across multiple services.

What is a spending mandate for AI agents?

A human-signed authorization defining what an agent can spend, where, and for how long. Once signed, the agent operates autonomously within those boundaries without per-transaction approval.

Can one agent identity work across multiple platforms?

Yes. A persistent Agent ID remains valid regardless of platform, framework, or wallet changes. FluxA's UPL resolves to the agent's current wallet automatically, preserving identity continuity.

What happens if an agent acts outside its mandate?

The payment is blocked before it clears. FluxA's risk control layer verifies host scope, remaining budget, and intent consistency at execution time — out-of-scope actions do not proceed.

How do merchants verify an agent transaction is legitimate?

Mastercard's Verifiable Intent issues tokenized credentials cryptographically linking each transaction to a human-approved spending mandate — specifying categories, caps, and time windows. FluxA Agent ID applies the same principle at the wallet layer.

Is agent identity a regulatory requirement yet?

Not formally — but NIST's AI Agent Standards Initiative, launched in February 2026, identifies agent security and identity as core pillars. Building compliant infrastructure now avoids retrofitting under future mandates.

FluxA is the payment infrastructure for AI agents, providing an AI co-wallet, virtual agent cards, the AEP2 stablecoin settlement protocol, MCP/API monetization, and built-in risk controls — so agents can pay, earn, and transact without human intervention.